A Closer Look at No Credit Check Commission Advances: What They Really Mean

In the competitive world of real estate, timing is everything. Closings are often weeks or months away, while expenses and personal financial obligations crop up daily. This dynamic drives many real estate agents and brokers to explore commission advances—tools that let professionals access a portion of their earned commissions prior to the closing date. As these services gain popularity, the concept of “no credit check commission advances” has become a buzzword in industry conversations. But what does it really mean to offer a commission advance with no credit impact? And what common misunderstandings need correction?

This in-depth guide is designed to demystify the term “no credit check commission advance” and clarify what’s truly evaluated in these transactions. We’ll explore how your credit score actually fits into the equation (if at all), break down what underwriters assess when approving a commission advance request, and address the biggest misperceptions—so you can make informed decisions about your real estate business’s cash flow, with compliance and peace of mind.

Understanding Commission Advances—The Non-Loan Reality

Before unpacking the nuances of credit checks, let’s clarify an even more fundamental point. A commission advance is not a loan. This distinction is crucial for compliance, industry transparency, and your own financial strategy.

A loan creates debt—you borrow money and commit to paying it back, often over months or years, with interest. In contrast, early access to commission through a commission advance is simply a purchase transaction. The advance company buys a portion of your earned, pending commission at a small discount, and you receive immediate funds. When the sale closes, your broker sends the agreed-upon portion of your commission to the commission advance company, fulfilling the transaction.

This structure matters because there’s no borrowing, no compounding interest, and—importantly for this conversation—no ongoing reporting to credit bureaus. The process doesn’t create a new credit obligation, which is where the “no credit check” claim begins to make sense.

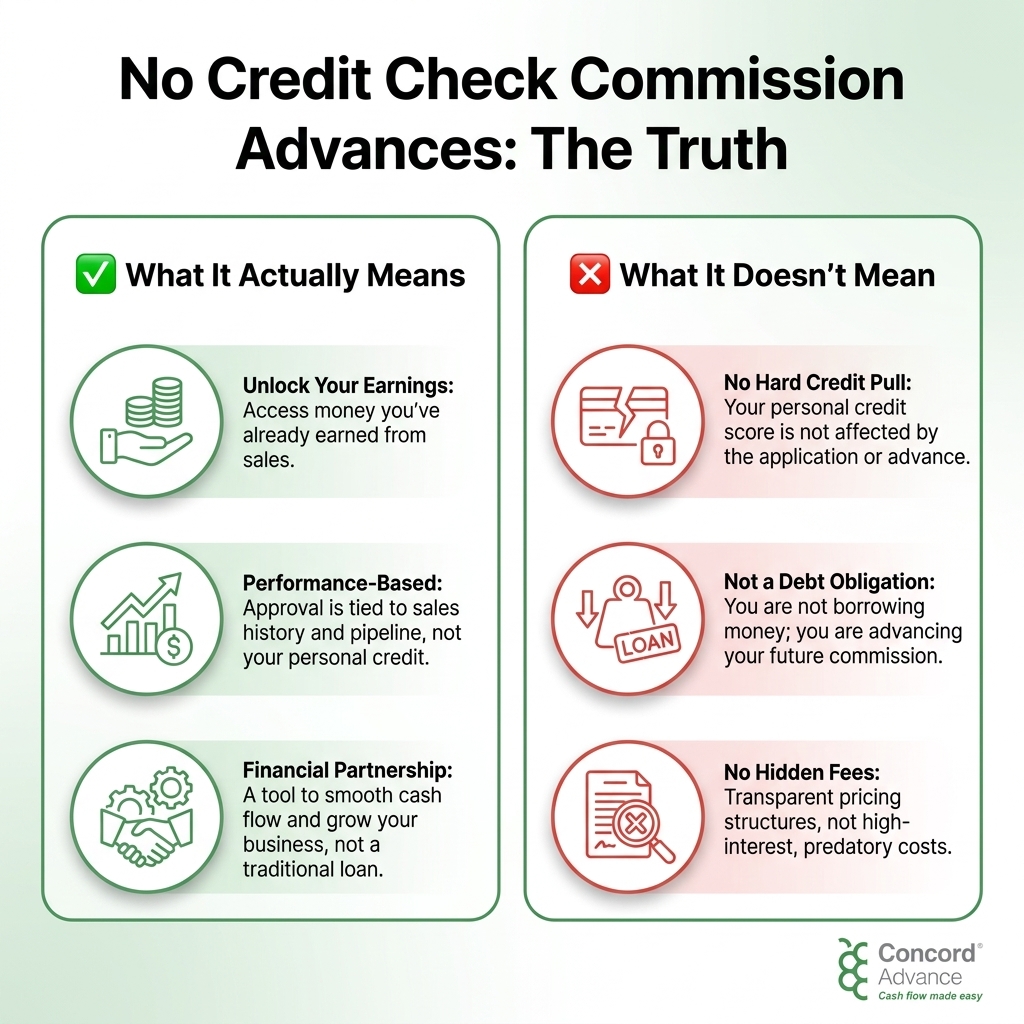

What Does “No Credit Check Commission Advance” Truly Mean?

At face value, the phrase suggests that your credit history, FICO score, or credit report won’t influence your eligibility. For real estate agents who may be new to the industry, self-employed, or rebuilding credit, this is attractive—after all, your credit score is one of your most sensitive financial assets.

But what’s actually happening behind the scenes? Is there really zero reliance on your personal credit?

The answer is both simple and a bit nuanced:

What’s Not Evaluated: Your Personal Credit, FICO Score, and Credit Report

For reputable commission advance providers, your personal credit does not factor into the advance approval decision. Applying does not generate a hard inquiry on your credit file, and the transaction does not appear as an installment or revolving account on your credit report.

In practice, this means:

- No hard credit pull: You will not see an inquiry appear on your credit bureau statement as a result of your commission advance application.

- No impact on FICO or VantageScore: Your score won’t drop due to the advance, either upon application or payoff.

- No new account reported: The advance does not show up as a loan, line of credit, or trade line on your credit files.

- No cumulative debt burden: Because the transaction is not a loan and involves no repayment in the traditional sense, your debt-to-income (DTI) ratio remains unaffected for future borrowing or qualifying processes.

What’s Actually Evaluated Instead?

If your individual credit isn’t considered, how does a commission advance provider decide to release funds? Approval focuses on the strength and details of the sale, not you. The primary factors evaluated include:

The Sales Contract: Underwriters closely review the signed purchase agreement. They want to see firm, executed deals, preferably with few contingencies, no red flags, and realistic close timelines. The cleaner and more confirmed the transaction, the more confidence they have.

Broker and Title Company Reputation: Advance companies may briefly review the transaction history of the broker or agency involved, especially if it’s a brokerage’s first time working with the advance provider. Title companies and escrow agents’ reliability are also considered.

Agent Track Record (to a Point): Some providers look at your history of past closed deals and any previous advances (if you’re a repeat client). However, this is more about verifying experience and reducing fraud risk than judging your personal finances or score.

Transaction Status: Underwriters seek evidence that the deal is well advanced—appraisals completed, financing stable, inspections done, and major milestones met. Deals with delayed closing dates or unaddressed contingencies may face higher scrutiny or advance limits.

This focus on the integrity of your earned commission, rather than your overall financial picture, is the defining feature of a truly “no credit check commission advance.” The transaction isn’t about lending money with risk based on your creditworthiness; it’s about enabling faster access to already-earned income from a sale that’s on track to close.

Dispelling Common Myths Around No Credit Check Commission Advances

Myth: No Credit Check Means No Evaluation At All

This is one of the biggest misunderstandings. “No credit check” simply means your personal credit history isn’t the basis for approval. It does not mean there is no screening process whatsoever. The provider will still want documentation that proves the sale is pending, addresses any potential risk, and ensures a legitimate business transaction. Think of it like a purchase agreement for future income, not an unsecured loan based on your past borrowing.

Myth: Commission Advances Can Help Build or Repair Credit

Because advances don’t show up on your credit report, they also cannot build, improve, or repair your credit score. They operate outside the traditional lending system. If credit-building is a primary goal, products designed for that purpose (like secured cards or credit-builder loans) remain the right fit.

Myth: Any Advance Advertised As “FICO Friendly” Carries Zero Risk

A “FICO friendly commission advance” means the arrangement doesn’t negatively affect your FICO score—it doesn’t leave a mark or create new debt. However, make sure you complete the transaction as agreed (the sale closes and the advance provider is paid from commission). Missing agreed-upon payments because a deal falls through can result in collection activity, though it still won’t show up as a direct mark on your score unless a judgment is later reported.

Myth: No Credit Check Advances Are Only for Struggling Agents

This is simply not the case. Many top agents and teams use commission advances strategically to smooth cash flow, fund marketing, pay vendors promptly, seize short-term opportunities, or reinvest in business growth. The “no credit check” feature is just as valuable for established professionals as those newer to the business.

Why Commission Advances Do Not Create Credit Implications

This subject is critically important in an age where credit health impacts everything from mortgage approvals to insurance premiums and even job opportunities. Here’s why commission advances deserve a category of their own:

Not Structured as a Loan: The advance is an upfront purchase of pending commission, not a loan repayment with a set amortization schedule or interest calculation.

No Credit Reporting: Commission advance providers do not report these transactions to the major credit bureaus, keeping your personal and business credit files untouched.

No Hard Inquiries: Unlike other forms of funding, applying doesn’t result in a “hard pull” which can ding your score (even temporarily).

Direct Repayment from Commission, Not Personal Bank Account: The funds are repaid automatically when your commission disburses after closing, not from a personal loan payment or auto-debit from your checking account.

FICO and VantageScore calculations are not triggered. Both scoring models rely on recorded credit obligations, repayment history, and available credit utilization—none of which are created by this transaction.

How the Commission Advance Application Process Really Works

Let’s walk through the steps, highlighting exactly where your credit standing is (and isn’t) involved:

Submit Application with Sales Contract Details: The application generally requires documentation of the in-contract sale, typically including the signed purchase agreement, commission disbursement details, and sometimes escrow/title information.

Simple Background and Transaction Review: The advance provider verifies the transaction, the legitimacy of the broker and, in some cases, the agent’s sales track record. Public records and fraud databases may be checked, but not your credit bureau file.

Underwriter Decision Based on Transaction Risk: Approval hinges on deal quality and downstream transaction partners—not FICO scores or revolving debt.

Terms Offered and Funds Released: Once approved, you select the commission amount you wish to access, agree to terms, provide any final required signatures or broker authorizations, and receive funds—often within 24-48 hours.

Repaid When Commission Pays Out: On closing day, the title company or brokerage deducts the advanced amount (and fee) and remits it directly to the advance provider. There is no payment out of your pocket or monthly installment to track.

Soft Pulls vs. Hard Pulls: When Is Your Credit Touched

Agents are increasingly sophisticated about credit. Some products in the wider financial world advertise “soft pull only” or “soft pull advance,” promising no hard inquiry on your credit report. Here, it’s vital to distinguish between products:

Commission advances from purpose-built providers do not even conduct a soft pull—they literally do not review your credit report, period. No inquiry shows, no points lost, no trace.

Other financial products (personal loans, lines of credit, or business cash advances) sometimes market themselves as “soft pull” at pre-qualification, but will later do a hard pull if you accept or close funding.

The distinction matters: A true no credit impact commission advance is by design invisible to your personal credit file throughout the entire process.

Why Are Credit Checks Skipped? The Business Logic

It’s worth asking: Why are commission advance companies able to skip credit checks, when nearly all other forms of funding require them? The answer lies in risk and collateral:

Deal-Oriented Risk: The provider’s risk is tied to the real estate transaction closing. If the deal falls through, their recourse is focused on recovering funds from forthcoming commissions, not from agent personal guarantees or assets.

No Ongoing Repayment: There are no fixed monthly payments to track or default on, since repayment happens on closing.

Transparent Fee-for-Service Structure: You’re not committing to a spreading interest charge or revolving utilization, just a one-time discount or fee taken from your earned commission.

Alternative Cash Flow, Not Parallel Credit: Commission advances aren’t a substitute for working capital loans, credit cards, or HELOCs. They fill a specific need—bridging the time between earning your commission and receiving your funds.

For these reasons, your credit health is simply outside the advance provider’s underwriting logic. Their model revolves around deal quality, not borrower profile.

What Happens If the Deal Falls Through?

Given the focus on transaction health over personal credit, what if a real estate sale unexpectedly collapses after an advance is released?

In this rare scenario, the advance provider will not report your missed repayment to credit bureaus as a loan default—because the advance was never a credit account to begin with. However, you and your broker are contractually obligated to ensure the advance is repaid from your next closing or, in some cases, from future earned commissions. Advance providers may seek repayment through other pending deals or engage in collection efforts if needed.

The process largely stays outside your credit file—unless the situation escalates to a legal judgment, which, if left unresolved and reported to public records, could eventually impact your credit. This is exceedingly rare and usually preventable through open communication with the provider.

Choosing a Commission Advance Company: Compliance, Trust, and Transparency

When evaluating commission advance companies, especially those advertising no credit check or FICO friendly commission advances, be mindful of the following best practices:

Look for Transparent Terms: The best providers clearly explain their fees, repayment structure, timelines, and documentation needs. Avoid companies that promise “guaranteed approval” without any verification of your pending transaction.

Recognize True Non-Credit Products: If the process requires your Social Security Number for a credit pull, or if the company discusses rates in APR or interest terms, you may not be dealing with a commission advance in the strictest sense.

Choose Providers with Experience in Your Brokerage Model: Some providers focus on independent agents, others serve large teams or franchise brokerages. Make sure the company understands your segment of the real estate industry and has a compliant, established process.

Prioritize Customer Service and Support: If something goes wrong in the deal (delayed close, transaction fallout), a reputable provider will guide you through next steps, update agreements, and seek fair solutions—not act as a typical lender or collections department.

How to Use Commission Advances Wisely for Business Growth

Commission advances, especially those with a genuine no credit impact, should be approached as a flexible business tool—not a last-resort option. Here are strategic ways that successful agents make the most of advance funding:

Invest in Marketing or Lead Generation: Secure funds before closing to launch new campaigns, order signs, or target premium listings.

Cover Bridge Expenses: Pay for staging, open house events, or necessary home repairs that your client or seller cannot cover upfront.

Smooth Out Cash Flow: Real estate is famously cyclical—advance funding helps you create more predictable, steady income month after month.

Seize Business Opportunities: Jump on time-sensitive coaching programs, mastermind groups, or technology upgrades that require upfront investment.

Pay Vendors and Staff Promptly: Maintain a reputation for reliability—vendors, contractors, and assistants stay loyal when you pay on time.

Sustain Personal Financial Health: Use advances as a short-term bridge to handle tax payments, health insurance, or family obligations, without dipping into savings or resorting to credit cards.

Compliance Reminder: Why You Shouldn’t Call It a “Loan”

One of the most important—and overlooked—compliance guidelines in commission advances is terminology. Never describe a commission advance as a “loan,” and avoid language around “borrowing” against your commission. Regulatory bodies and professional associations are clear: Calling an advance a loan could require adherence to consumer lending laws, disclosures, and state-level licensing you don’t need for a purchase-and-sales transaction.

Educational outreach from NAR (National Association of Realtors®), industry attorneys, and trusted brokerages all reinforce this point. Stay compliant and protect your business by using the right language—early access to already-earned commission, commission purchasing, or advance funding for pending sales.

Frequently Asked Questions About No Credit Check Commission Advances

Is There Any Circumstance Where My Credit Is Reviewed?

In standard commission advance transactions from reputable companies, your credit will not be checked or reported. If you’re offered a product with “advance” in the title but are required to consent to a credit inquiry, clarify the product type and seek alternative providers.

Can I Get Multiple Advances at Once?

You can often access advances on multiple separate pending transactions, as long as each sale independently qualifies and there are no overlapping advance requests on the same commission. The provider may review your past advance history for risk, but not your credit file.

Can Newer Agents Qualify for No Credit Check Commission Advances?

Yes. The process does not assume a robust credit history or high FICO score. Approval hinges on having a valid, in-contract sale and a participating brokerage.

Are Fees Higher Without Credit Checks?

No. The fees (or discount rate) for most commission advances are determined by transaction risk (date to close, broker reputation, etc.), not by your credit profile. You are not penalized for credit inexperience or a short credit history.

How Fast Is the Process?

Many commission advance companies can fund within 24-48 hours of application approval, allowing agents to move quickly on essential expenses or investments.

Key Takeaways: Making the Most of No Credit Impact Commission Advances

The allure of commission advance products that promise no credit check is strong, and for good reason—your credit is a cornerstone of financial health as a real estate professional. But the real story is both simpler and more reassuring than you might expect.

Commission advances designed for real estate agents, teams, and brokers operate entirely outside the world of credit. Instead of scrutinizing your FICO score, these providers focus on the viability and security of your earned sale. The application, underwriting, and repayment all revolve around the transaction—not your personal finances.

This unique arrangement empowers you to access funds flexibly and quickly, without adding debt or risking your score. Used wisely, no credit check commission advances can be a powerful bridge to business growth, cash flow stability, and peace of mind in an unpredictable industry.

Always verify you’re working with a transparent, reputable provider, and remember: early access to commission isn’t borrowing—it’s unlocking your own earnings, on your schedule, with no credit strings attached. That’s what “no credit check commission advance” really means.