What Is a Real Estate Commission Advance?

A real estate commission advance is a financial service that allows agents and brokers to access a portion of their earned commission before a transaction officially closes.

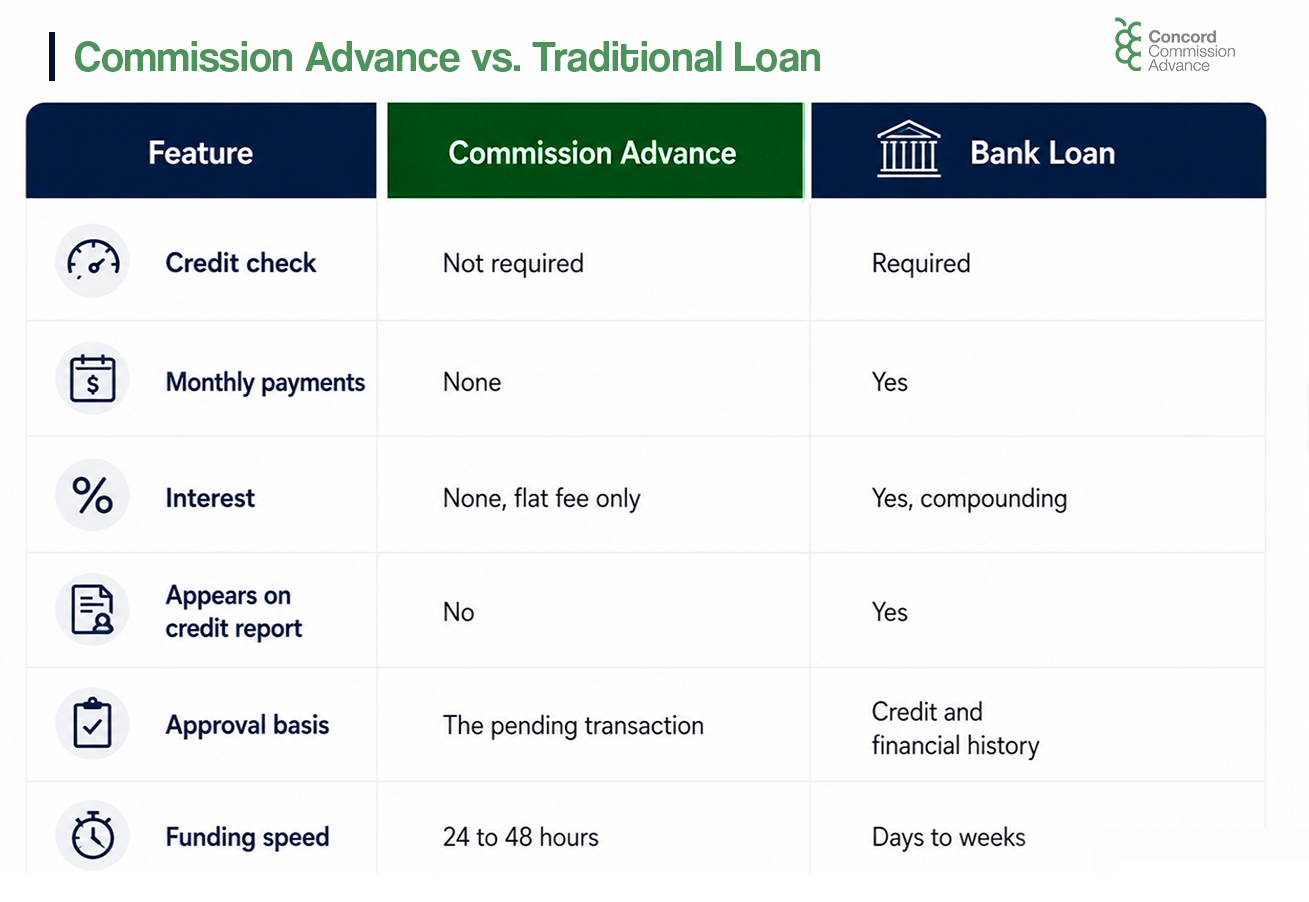

The advance company pays the agent a portion of the expected commission upfront in exchange for a small flat fee. At closing, the advance company takes what it is owed from the commission, and the agent receives the remainder.

Key Takeaways

- A commission advance gives agents early access to commissions on pending transactions.

- It is structured as a receivables purchase, not a loan.

- Approval is based entirely on the strength of the pending transaction.

- Repayment happens automatically at closing.

- Fees are flat and disclosed upfront.

How the Process Works

- Application: The agent submits a short online application with the details of the pending transaction: the property address, expected closing date, and net commission amount.

- Verification: The advance company reviews the signed purchase agreement and confirms the transaction details. Eligibility is determined by the strength of the deal instead of the agent’s financial history.

- Broker approval: Commissions are legally disbursed through the broker. The broker signs a brief agreement directing the advanced amount to the advance company at closing. Most brokers are familiar with this step and complete it routinely. In some states or circumstances, the title or escrow company signs in place of the broker.

- Funding: Once approved, funds are deposited directly into the agent’s bank account typically within 24 to 48 business hours.

- Repayment: At closing, the advance amount plus the flat fee is sent directly to the advance company from the commission disbursement.

What Does It Cost?

Commission advance fees are percentage-based fees of the advance amount, typically ranging from 5% to 15%, depending on the advance size and the expected closing timeline.

Example: An agent with a $12,000 net commission requests an $8,000 advance at a 10% fee. The agent receives $7,200 upfront. At closing, $8,000 is directed to the advance company. The remaining $4,000 is disbursed to the agent as usual. Total cost: $800 for immediate access to $7,200 in working capital.

Because a commission advance is a receivables purchase and not a debt instrument, it does not affect an agent’s debt-to-income ratio or ability to qualify for personal financing. This distinction carries practical significance for agents who are also managing a mortgage application or other credit obligations.

Who Qualifies?

Eligibility is based entirely on the pending transaction. An agent generally qualifies when the following are in place:

- Active real estate license

- Signed purchase agreement on a pending transaction

- Confirmed expected closing date

- Verifiable net commission amount

- Broker willing to direct the commission at closing

Credit score, income history, and years of experience play no role in the approval decision.

What Happens If the Deal Falls Through?

When a transaction does not close after an advance has been issued, the agent is typically not required to repay the amount immediately out of pocket. Most advance companies work with the agent to recover the funds from a subsequent closed transaction.

The broker bears no personal financial liability in this scenario. If an agent earns no future commissions or departs the brokerage, the broker is not responsible for the outstanding balance.

The Bottom Line

A real estate commission advance is a straightforward financial tool that gives agents control over the timing of their income. It does not create debt, does not require strong credit, and places no financial risk on the broker. The cost is a flat, transparent fee, disclosed before any agreement is signed.

For agents navigating the natural cash flow gaps of a commission-based career, it remains one of the most practical and accessible options available.

Concord Advance provides commission advances to residential and commercial real estate agents nationwide. Applications are completed online at concordadvance.com.

Frequently Asked Questions

1. Can a newly licensed agent apply for commission advance?

Yes, as long as an agent holds an active license and has a signed purchase agreement on a pending deal. Years of experience and income history are not factors. A first-year agent with a contract under way is eligible for advances.

2. How Should agents compare different commission advance providers?

Agents should evaluate total fees, funding speed, transparency of terms, geographic coverage, minimum transaction requirements, customer support, broker involvement, and whether fees increase if a transaction is delayed.

3. How do commission advance companies evaluate the risk of a transaction?

Providers typically review the purchase contract, financing status, contingency periods, title progress, closing schedule, brokerage verification, and commission structure. Transactions that are further along in the closing process generally present lower risk than newly executed contracts.